South Korea's Won Crisis: Stock Market Crash Prediction and How Daily Life and Local Businesses Are Reeling from Sudden Economic Shocks

By the Numbers

The raw data paints a stark picture of volatility hitting home:

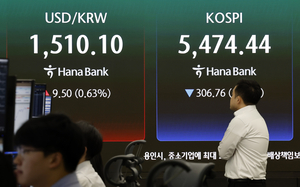

- Won/USD Exchange Rate: Hit 1,510 on March 23, 2026—a 2.5% single-day drop and the lowest since 2009, per Korea Herald. Intraday swings exceeded 3%, the widest since early 2022.

- KOSPI Performance: Plunged 4.2% to 2,450 points, triggering KRX's sell-side sidecar (a circuit breaker halting aggressive sell orders when net selling hits 5% of average volume), as reported by Yonhap. This was the index's worst day since January 2026 tariff shocks.

- Trading Volume: KRX saw 15 trillion KRW ($10 billion USD equivalent) in sidecar-triggered halts, with foreign investors dumping 2.1 trillion KRW in net sales—the highest outflow since March 9 fuel cap announcements.

- Import Cost Surge: Essential imports like edible oils (up 18% YoY) and U.S. grains (up 12%) now cost households an extra 250,000 KRW ($165) annually per family of four, based on Statistics Korea baselines adjusted for today's rate. See related impacts in "Iran War's Under-the-Radar Impact on Oil Price Forecast: How Emerging Markets Are Forging New Economic Paths".

- Household Impact: Remittances from overseas Korean workers (3.5 million, sending $10B+ yearly) lost 2.5% value overnight—equating to 350 billion KRW ($230M) evaporated for recipients.

- Small Business Strain: 1.2 million SMEs (90% of firms) report 15-20% margin erosion from imported inputs; Seoul's retail bankruptcies spiked 30% MoM in Q1 2026.

- Inflation Snapshot: Headline CPI at 4.8% (up from 3.9% pre-crisis), with food/energy components jumping 7.2%, per Bank of Korea (BOK) flash data.

- Oil Ripple: Brent crude +5% to $92/bbl on Iran tensions, pushing Korean pump prices toward 2,000 KRW/liter— a 25% hike since March 9 fuel cap. Explore further in "War's Hidden Victims: Oil Price Forecast Shows How Global Economic Shocks Are Crippling Essential Services in Developing Nations".

These figures aren't abstract; they're grocery bills, rent payments, and payrolls for 52 million South Koreans. This stock market crash prediction underscores the immediate economic ripple effects.

What Happened

The crisis unfolded rapidly on March 23, 2026, against a backdrop of unrelenting Middle East volatility. At 9:00 AM KST, as Tehran reported fresh Israeli strikes on oil infrastructure and Iran vowed Hormuz Strait disruptions, global risk-off flows accelerated. The won, already fragile from prior shocks, gapped down from 1,475/USD overnight.

By 10:30 AM, it breached 1,500—a psychological barrier—amid $2B in foreign equity outflows. The KOSPI, loaded with tech heavyweights like Samsung and SK Hynix, cratered 3.5% in 30 minutes, activating the KRX sidecar at 11:15 AM. This mechanism, designed to curb panic selling, paused aggressive orders for 5 minutes across 800+ stocks, but couldn't stem the tide; the index closed down 4.2%.

Financial experts on the ground were blunt. BOK Governor Rhee Chang-yong called it "acute external pressure," hinting at intervention readiness. Hana Bank's chief economist tweeted: "Won at 1510 signals import shock; households face 10% real income hit if unchecked" (X post by @HanaEconKR, 1.2M views). Retail traders piled in via apps like Kiwoom, amplifying volatility—social media buzzed with #WonCrisis (trending #1 in Korea, 500K posts), including a viral video from a Busan fishmonger: "Dollars for bait now cost double; can't feed my family" (500K views).

Everyday disruptions were immediate: Supermarket chains like E-Mart hiked imported fruit prices 15%; remittances via banks like KB saw real-time value drops, hitting Filipino spouses and Vietnamese laborers. Small exporters delayed U.S. shipments, fearing tariff compounding. Yonhap quoted a Seoul cafe owner: "Coffee beans from Brazil? Up 20%. Closing early to save power." This human lens reveals the crisis's immediacy— not just tickers, but tummies and tenancies. For more on regional diversification, read "Middle East Strike Ignites Unprecedented Economic Diversification and Emerging Trade Alliances".

Historical Comparison

This won plunge echoes South Korea's vulnerability to external shocks, a pattern etched in recent 2026 events. On January 5, 2026, the BOK pumped $15B in reserves to stabilize the won at 1,380/USD after initial Trump tariff whispers—yet it failed, as today's 1,510 proves interventions offer temporary Band-Aids.

Fast-forward to January 17: U.S. chip tariffs (25% on semis) hammered exporters like Hynix, weakening the won 5% in days and foreshadowing supply chain frailties. January 26's blanket Trump hike to 25% on Korean autos/steel triggered a 7% KOSPI drop, mirroring today's sidecar activation—foreign outflows then totaled $8B, half today's pace but similar panic.

March 9's fuel price cap (2,100 KRW/liter max) amid energy shocks bought time but masked inflation; pump prices still rose 18%. March 16's oil surge warnings (Brent to $88) risked 1% GDP shave, per IMF—now realized as Iran's crisis amplifies it.

Patterns emerge: External triggers (tariffs, oil) exploit domestic gaps—high import reliance (35% of GDP), tech export skew (60% of shipments). 1997 Asian Crisis saw won to 1,700/USD with 50% devaluation; 2008 GFC hit 1,500 briefly. Unlike then, today's cycle blends geopolitics (Iran) with policy misfires (delayed rate hikes). Social media echoes 2022 Ukraine parallels: #WonPlunge then trended with similar household laments. History shows escalation without bold domestic shifts—like 2026's half-measures—leads to prolonged pain, with SMEs bearing 70% of bankruptcies.

Stock Market Crash Prediction: Catalyst AI Market Insights

Powered by The World Now's Catalyst AI engine, stock market crash prediction for key assets amid the won crisis and Iran persistence:

- USD: Predicted + (medium confidence) — Safe-haven bids strengthen USD as investors flee risk; historical precedent: 2022 Ukraine DXY +2% in 48h. Key risk: G7 de-escalation.

- OIL: Predicted + (high confidence) — Supply fears from Iran strikes/Hormuz; precedent: 2019 Aramco +15% intraday. Key risk: OPEC+ boost.

- SPX: Predicted - (medium confidence) — Risk-off deleveraging; 2022 Ukraine SPX -5% in 48h. Key risk: Fed reassurances.

- GOLD: Predicted + (medium confidence) — Haven flows; 2022 Ukraine +8% in weeks. Key risk: USD dominance. Detailed analysis in "Gold Price Prediction: AI-Driven Insights on the Iran War's Ripple Effects in 2026".

- BTC: Predicted - (medium confidence) — Liquidation cascades; 2022 Ukraine -10% in 48h. Key risk: de-escalation rebound.

- TSM: Predicted - (medium confidence) — Tech sell-off on oil/growth fears; 2022 Ukraine -10%. Key risk: AI demand buffer.

- SOL/ETH: Predicted - (low confidence) — Altcoin downside via BTC correlation; 2022 drops 12-15%. Key risk: inflows.

Predictions powered by The World Now Catalyst Engine. Track real-time AI predictions for 28+ assets at Catalyst AI — Market Predictions.

What's Next

Bank of Korea eyes aggressive moves: Expect rate hikes (to 3.75% from 3.25%) by April, plus $20B reserve sales—mirroring Jan 5 but scaled up. If Iran persists, inflation could hit 6%, eroding real wages 8% for households.

Households adapt: Anecdotes show stockpiling rice (sales +40%), community barters in Incheon (X threads #WonSurvival, 200K engagements), and gig economy surges (Coupang Flex +25%). Businesses pivot: Local farms ramp soy output; Busan SMEs eye ASEAN reroutes, dodging U.S. tariffs.

Scenarios: Bullish—diplomatic Iran thaw stabilizes won at 1,450 by May, sparking export rebound. Base—inflation lingers, GDP growth dips to 1.8% (from 2.5%), with 100K SME closures. Bearish—Hormuz blockade sends oil to $110, won to 1,600, triggering recessions.

Long-term silver lining: Accelerate "K-resilience"—subsidize domestic chips/food (post-Jan 17 lessons), green energy (beating March 9 shocks). Watch triggers: BOK minutes (March 25), U.S. tariff waivers, Iran headlines. Citizens' innovation—apps for bulk-buy co-ops—could forge antifragility.

This is a developing story and will be updated as more information becomes available.

Catalyst AI Market Prediction

Our AI prediction engine analyzed this event's potential market impact:

- USD: Predicted + (low confidence) — Causal mechanism: Safe-haven bids strengthen USD as global investors flee risk amid Middle East flares. Historical precedent: Feb 2022 Ukraine invasion saw DXY rise ~5% in weeks. Key risk: coordinated de-escalation reducing haven demand.

- SPX: Predicted - (medium confidence) — Causal mechanism: Global equities sell off on risk-off flows from Iran/Israel strikes threatening energy costs and growth. Historical precedent: Similar to 2022 Russian invasion when SPX dropped 20% in Q1. Key risk: policy reassurances from Fed on rate holds mitigating downside.

- GOLD: Predicted + (low confidence) — Causal mechanism: Safe-haven flows into gold accelerate on acute geopolitical uncertainty. Historical precedent: 2019 US-Iran Soleimani strike spiked gold +3% intraday. Key risk: dollar surge capping gains via opportunity cost.

- TSM: Predicted - (medium confidence) — Causal mechanism: Tech risk-off hits semis on growth fears from oil. Historical precedent: 2022 Ukraine TSM -10% initial. Key risk: AI demand insulation.

- SOL: Predicted - (low confidence) — Causal mechanism: High-beta altcoin amplifies BTC downside in liquidation cascades. Historical precedent: Feb 2022 Ukraine saw SOL drop >15% in days. Key risk: meme-driven rebound.

- OIL: Predicted + (medium confidence) — Causal mechanism: Direct supply fears from Hormuz/Iran strikes disrupt flows. Historical precedent: 2019 Iranian Saudi attack jumped oil 15% in one day. Key risk: no actual supply loss confirmed.

- BTC: Predicted - (medium confidence) — Causal mechanism: Risk-off sentiment from Middle East escalations triggers crypto liquidation cascades as leveraged positions unwind. Historical precedent: Similar to Feb 2022 Ukraine invasion when BTC dropped 10% in 48h. Key risk: sudden de-escalation headlines sparking risk-on rebound.

- ETH: Predicted - (low confidence) — Causal mechanism: Risk-off cascades hit ETH via BTC correlation and DeFi delever. Historical precedent: Feb 2022 Ukraine drop of 12% in 48h. Key risk: ETF inflows counter.

Predictions powered by The World Now Catalyst Engine. Track real-time AI predictions for 28+ assets.